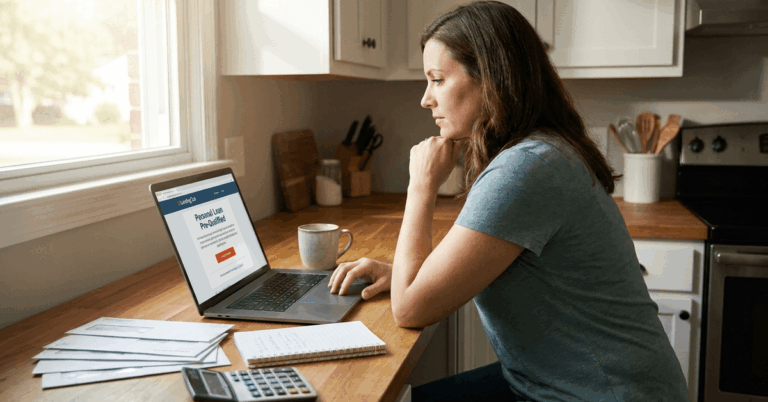

Managing multiple credit cards with high interest rates can be overwhelming. Many people searching for relief wonder about ways to simplify balances, lower rates, and clear debt faster.

For anyone struggling with credit card bills, the thought of handling just one payment a month—often at a lower interest rate—sounds pretty appealing. That’s where personal loans from digital lenders like SoFi might help.

Understanding Credit Card Debt and Its Impact

Credit card debt tends to creep up silently over time. Most cards carry variable, relatively high APRs—sometimes above 20%. If monthly payments only cover the minimum, it could take years to pay off a balance.

The result is a cycle of compounding interest that’s tough to escape. A personal loan, especially from a lender with decent rates, can offer a possible solution that’s straightforward and potentially less stressful.

What Is Refinancing Credit Card Debt with a Personal Loan?

When refinancing, a borrower takes out a new loan (usually an installment loan) to pay off one or more higher-interest credit card balances. Instead of juggling several cards, you make a single, fixed payment each month over a set period.

Financially, it can mean lower interest paid overall and a definite end date for your debt, something not always guaranteed with revolving credit.

Why Use a Personal Loan for Refinancing?

People looking for alternatives to traditional bank loans or balance transfers sometimes find personal loans appealing because:

- Rates are often lower than credit card APRs for well-qualified borrowers

- Terms are fixed, so payments—and the payoff timeline—are predictable

- Application processes with online lenders like SoFi can be fast and convenient

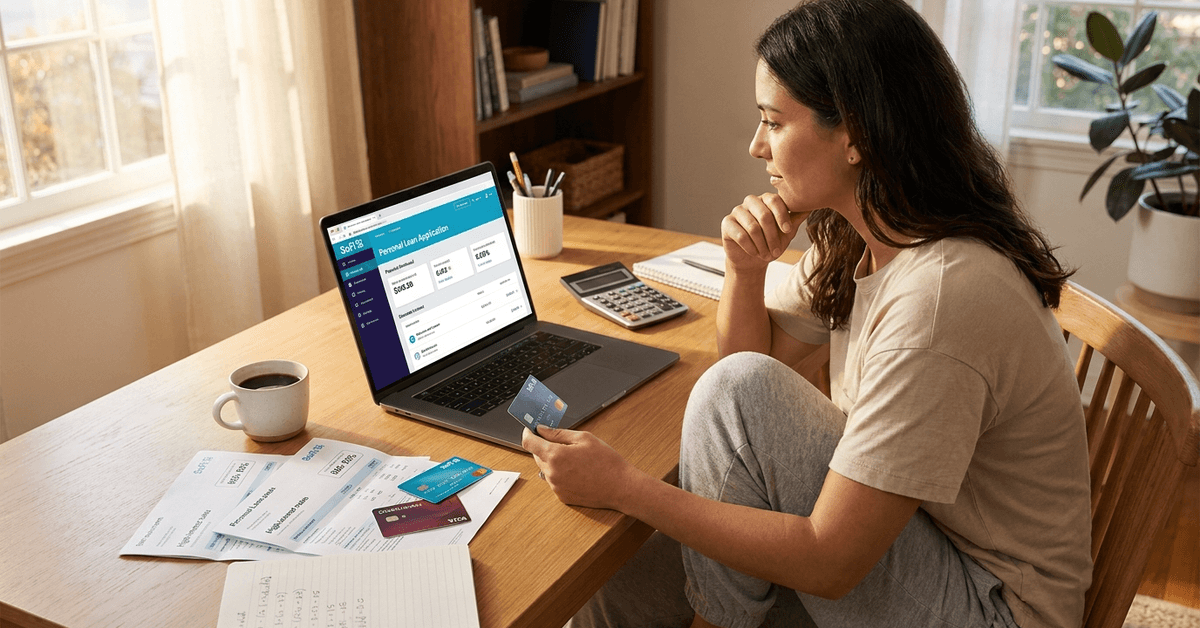

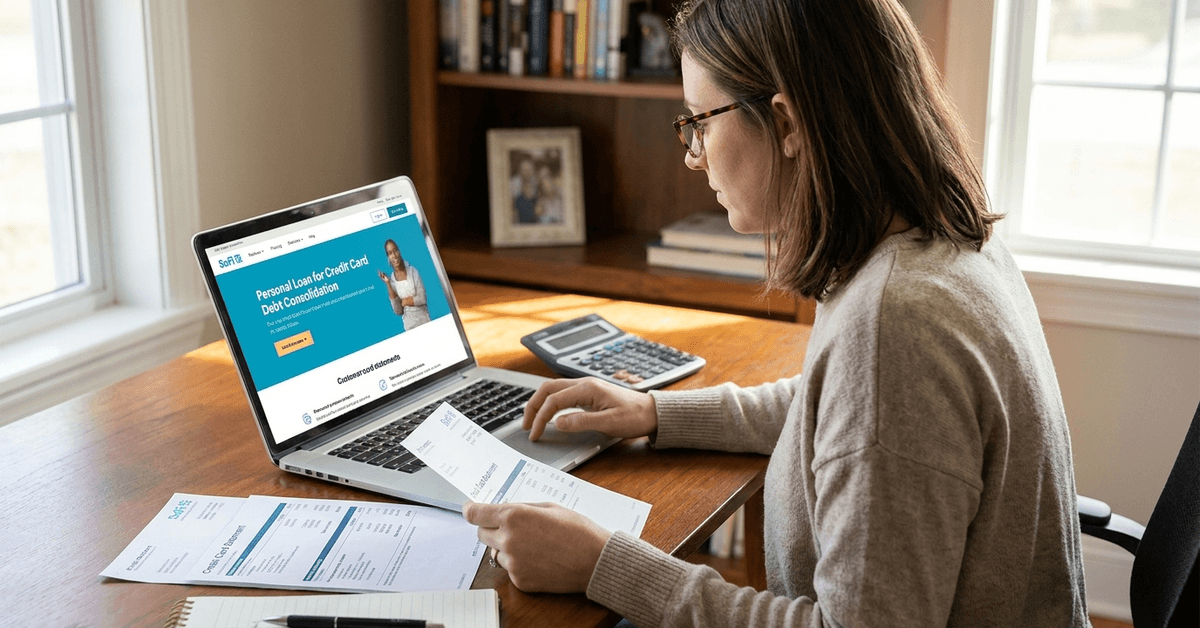

How SoFi Personal Loans Work for Debt Refinancing

SoFi offers unsecured personal loans that can be used for a number of purposes, including credit card consolidation.

Applicants typically receive a decision quickly after applying online. If approved, the funds can pay off existing credit card balances, consolidating everything into a single loan.

SoFi Personal Loan Features

- No origination or prepayment fees

- Fixed APRs and flexible repayment terms

- Loan amounts typically range from $5,000 to $100,000

- Rate discounts may be available with autopay

I’ve noticed a few people mention the process is less intimidating than contacting a local bank, possibly due to SoFi’s digital-first platform.

It’s hard to say if that experience is universal, but online reviews often highlight quick funding and easy account management.

Potential Benefits of Refinancing with a SoFi Personal Loan

Lower Interest Rates

Many credit cards carry double-digit rates. By refinancing with a loan that has a lower, fixed APR, you could potentially save a fair bit on interest over time.

Simpler Repayment Structure

Having just one monthly payment is easier to track. It may reduce the risk of late payments and penalties, especially if you routinely manage multiple accounts.

Fixed Timeline for Repayment

Unlike revolving credit, most personal loans have a clear end date. This can help some people stay motivated, because there’s a real sense of progress as the balance drops each month.

Boost to Credit Mix

Credit bureaus look at the variety of debt in your profile. Adding an installment loan (such as a personal loan) alongside credit cards broadens your credit mix, which might give your score a nudge—if all payments are made on time, of course.

Drawbacks and Considerations of Refinancing Credit Card Debt

There are advantages, but it isn’t a universal fix. Perhaps the main thing to keep in mind: Refinancing moves debt around; it doesn’t erase it.

After using a loan to pay off cards, some people might run up new charges. That’s a real risk, especially if spending habits haven’t changed.

Potential for New Debt

Once cards are paid off, keeping them open with $0 balances can help your credit—yet there’s a temptation to use them again. It’s worth reflecting on whether your spending might creep back up if those credit lines remain open and accessible.

Loan Approval Requirements

Qualifying for the best rates typically requires solid credit. SoFi highlights a minimum credit score, verifiable income, and other standard checks. Not everyone will see the lowest advertised rates, especially if their credit is only fair.

Monthly Payment May Be Higher

While you might pay less overall in interest, a personal loan often requires a larger monthly payment than making minimum card payments. This can tighten your budget, unless you factor in the long-term savings.

Application Process for a SoFi Personal Loan

Research and Compare

It’s wise to compare several lenders. While SoFi might be well-known for digital convenience and transparent terms, it never hurts to see what other platforms could offer, especially in terms of rates and customer service.

Check Your Rate with Soft Credit Inquiry

The initial rate check doesn’t usually impact your credit score, which is helpful. You can understand possible rates and terms before committing to a full application.

Complete the Online Application

Applicants provide some personal and financial information, including proof of employment or income. Approvals may be nearly instant in some cases, with funding to your bank in a few days if all documents are in order.

Tips for Successfully Refinancing Credit Card Debt

- Calculate the total amount needed to fully pay off all cards—don’t underestimate.

- Factor in your new payment with your current monthly budget to avoid a cash crunch.

- Plan how you’ll use your old credit cards after consolidation; responsible management helps your credit profile.

Legal, Tax, and Consumer Protection Considerations

Understanding the Agreement

It’s important to review all loan terms carefully. Reading the fine print can highlight possible fees or penalties—even if SoFi is upfront about its pricing, other lenders sometimes aren’t.

Checking for Prepayment Penalties

SoFi does not charge these, but it’s not an industry standard. Early payoff can help some borrowers save even more in interest if allowed.

Credit Score Monitoring

Applying for credit and consolidating debt impacts your credit score in the short term, sometimes dropping it a few points. Over time, consistent, on-time payments may improve your score, but tracking your credit can provide extra assurance during the process.

Frequently Asked Questions about Refinancing with SoFi

Does refinancing with a personal loan hurt my credit?

Applying could temporarily drop your score, but responsible repayment typically helps scores recover and grow over time.

Can I refinance more than once?

Possible, but it isn’t recommended unless the new loan terms are better overall. Regular refinancing can signal risk to lenders.

Are there alternatives to personal loans for credit card consolidation?

Some consumers use balance transfer cards, home equity loans, or credit counseling services. Each comes with pros and cons worth considering.

Final Thoughts on SoFi Credit Card Debt Refinancing

Refinancing credit card debt with a SoFi personal loan can help simplify payments and create a clearer payoff timeline. A fixed loan may reduce interest costs for qualified borrowers, but it still requires careful budgeting and consistent repayment.

Since approval, rates, and monthly payments depend on your credit profile and income, comparing options before applying is important.

With responsible spending habits and a clear debt plan, refinancing can be a practical step toward better financial control.